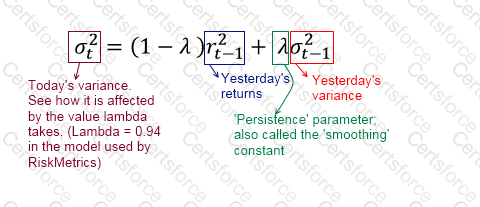

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter λ = 0.93.

Loss from a lawsuit from an employee due to physical harm caused while at work is categorized per Basel II as:

For a given mean, which distribution would you prefer for frequency modeling where operational risk events are considered dependent, or in other words are seen as clustering together (as opposed to being independent)?

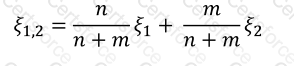

For a hypotherical UoM, the number of losses in two non-overlapping datasets is 24 and 32 respectively. The Pareto tail parameters for the two datasets calculated using the maximum likelihood estimation method are 2 and 3. What is an estimate of the tail parameter of the combined dataset?

Which of the following statements are true:

I. It is usual to set a very high confidence level when estimating VaR for capital requirements.

II. For model validation, very high VaR confidence levels are used to minimize excess losses.

III. For limit setting for managing day to day positions, it is usual to set VaR confidence levels that are neither too low to be exceeded too often, nor too high as to be never exceeded.

IV. The Basel accord requirements for market risk capital require the use of a time horizon of 1 year.

A risk management function is best organized as:

According to the Basel framework, reserves resulting from the upward revaluation of assets are considered a part of:

If the marginal probabilities of default for a corporate bond for years 1, 2 and 3 are 2%, 3% and 4% respectively, what is the cumulative probability of default at the end of year 3?

Which of the following statements are true ?

I. Risk governance structures distribute rights and responsibilities among stakeholders in the corporation

II. Cybernetics is the multidisciplinary study of cyber risk and control systems underlying information systems in an organization

III. Corporate governance is a subset of the larger subject of risk governance

IV. The Cadbury report was issued in the early 90s and was one of the early frameworks for corporate governance

Which of the following is not a possible early warning indicator in relation to the health of a counterparty?