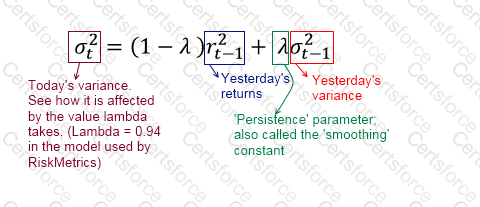

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter λ = 0.93.

Recall the formula for calculating variance under EWMA. See below. Therefore the correct answer is =SQRT((1 - 0.93)*(LN(11/10))^2 + 0.93*((3.5%^2))) = 4.21%. Other answers are incorrect. Note that continuous returns are to be used, ie ln(11/10) and not discrete returns (=1/10) - though generally the difference between the two is small over short time periods. (If in the exam the answer doesn't exactly match, try using discrete returns.)

Contribute your Thoughts:

Chosen Answer:

This is a voting comment (?). You can switch to a simple comment. It is better to Upvote an existing comment if you don't have anything to add.

Submit