What percentage of average annual gross income is to be held as capital for operational risk under the basic indicator approach specified under Basel II?

Which of the following statements are true:

I. Stress tests should consider simultaneous pressures in funding and asset markets, and the impact of a reduction in liquidity

II. Judging the effectiveness of risk mitigation techniques is not a part of stress testing

III. A reverse stress test is useful for discovering hidden vulnerabilities and inconsistencies in hedging strategies

IV. Reputational risk, which is explicitly excluded from the definition of operational risk under Basel II, should still be considered as part of stress tests.

Which of the following statements is true:

I. Recovery rate assumptions can be easily made fairly accurately given past data available from credit rating agencies.

II. Recovery rate assumptions are difficult to make given the effect of the business cycle, nature of the industry and multiple other factors difficult to model.

III. The standard deviation of observed recovery rates is generally very high, making any estimate likely to differ significantly from realized recovery rates.

IV. Estimation errors for recovery rates are not a concern as they are not directionally biased and will cancel each other out over time.

For credit risk calculations, correlation between the asset values of two issuers is often proxied with:

Which of the following statements is true in relation to a normal mixture distribution:

I. The mixture will always have a kurtosis greater than a normal distribution with the same mean and variance

II. A normal mixture density function is derived by summing two or more normal distributions

III. VaR estimates for normal mixtures can be calculated using a closed form analytic formula

The standalone economic capital estimates for the three uncorrelated business units of a bank are $100, $200 and $150 respectively. What is the combined economic capital for the bank?

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds over a one year horizon are 0.03 and 0.08 respectively. If the default correlation is zero, what is the one year expected loss on this portfolio?

Under the KMV Moody's approach to calculating expecting default frequencies (EDF), firms' default on obligations is likely when:

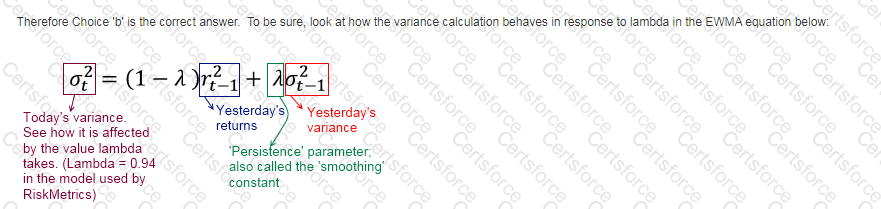

As the persistence parameter under EWMA is lowered, which of the following would be true:

Which of the following statements are true:

I. Shocks to risk factors should be relative rather than absolute if we wish to avoid a change in the sign of the risk factor.

II. Interest rate shocks are generally modeled as absolute shocks.

III. Shocks to volatility are generally modeled as absolute shocks.

IV. Shocks to market spreads are generally modeled as relative shocks.