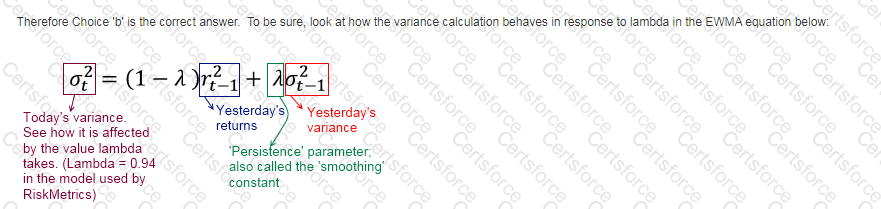

The persistence parameter, λ, is the coefficient of the prior day's variance in EWMA calculations. A higher value of the persistence parameter tends to 'persist' the prior value of variance for longer. Consider an extreme example - if the persistence parameter is equal to 1, the variance under EWMA will never change in response to returns.

1 - λ is the coefficient of recent market returns. As λ is lowered, 1 - λ increases, giving a greater weight to recent market returns or shocks. Therefore, as λ is lowered, the model will react faster to market shocks and give higher weights to recent returns, and at the same time reduce the weight on prior variance which will tend to persist for a shorter period.

Contribute your Thoughts:

Chosen Answer:

This is a voting comment (?). You can switch to a simple comment. It is better to Upvote an existing comment if you don't have anything to add.

Submit