Which of the following risks were not covered in detail in most stress tests prior to the current crisis:

I. The behavior of complex structured products under stressed liquidity conditions

II. Pipeline or securitization risk

III. Basis risk in relation to hedging strategies

IV. Counterparty credit risk

V. Contingent risks

VI. Funding liquidity risk

Under the internal ratings based approach for risk weighted assets, for which of the following parameters must each institution make internal estimates (as opposed to relying upon values determined by a national supervisor):

Which of the following credit risk models considers debt as including a put option on the firm's assets to assess credit risk?

Random recovery rates in respect of credit risk can be modeled using:

Which of the following statements are true:

I. Credit risk and counterparty risk are synonymous

II. Counterparty risk is the contingent risk from a counterparty's default in derivative transactions

III. Counterparty risk is the risk of a loan default or the risk from moneys lent directly

IV. The exposure at default is difficult to estimate for credit risk as it depends upon market movements

According to the Basel II framework, subordinated term debt that was originally issued 4 years ago with a maturity of 6 years is considered a part of:

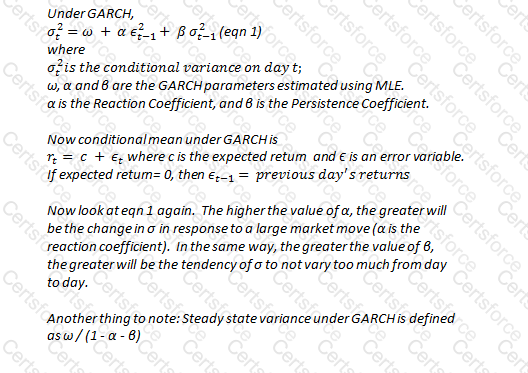

What is the annualized steady state volatility under a GARCH model where alpha is 0.1, beta is 0.8 and omega is 0.00025?

Which of the following are considered asset based credit enhancements?

I. Collateral

II. Credit default swaps

III. Close out netting arrangements

IV. Cash reserves

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

As opposed to traditional accounting based measures, risk adjusted performance measures use which of the following approaches to measure performance: