Steady state variance under the GARCH model is given by the formula ω/(1 - α – β). In this case, steady state variance therefore works out to 0.00025/(1 - 0.1 - 0.8) = 0.0025. Since this is the variance, volatility is the square root of 0.0025, which works out to 0.05.

Thus, 5% (=0.05) is the correct answer, and the others are incorrect.

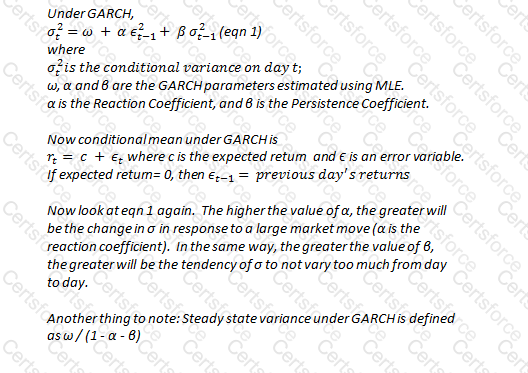

Also recall the following in respect of GARCH:

Contribute your Thoughts:

Chosen Answer:

This is a voting comment (?). You can switch to a simple comment. It is better to Upvote an existing comment if you don't have anything to add.

Submit