A company enters into a floating rate borrowing with interest due every 12 months over the five year life of the borrowing.

At the same time, the company arranges an interest rate swap to swap the interest profile on the borrowing from floating to fixed rate.

These transactions are designated as a hedge for hedge accounting purposes under IAS 39 Financial Instruments: Recognition and Measurement.

Assuming the hedge is considered to be effective, how would the swap be accounted for 12 months later?

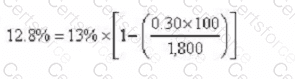

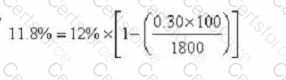

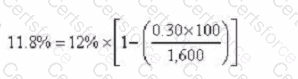

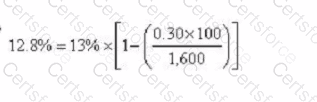

Company M is a geared company whose equity has a market value of $1,500 million and debt has a market value of S300 million. The company plans to issue $200 million of new shares and use the funds raised to pay off some of the debt

Company M currently has a cost of equity of 13% and a WACC of 10% It pays corporate tax at the rate of 30% Company B, an ungeared company operating in the same business sector as Company M, has a cost of equity of 12%

Assume Modigliani and Miller's theory of capital structure with tax applies

Which calculation below shows the correct approach to calculating the new WACC following the planned changes in capital structure?

A

B

C

D

VVV has a floating rate loan that it wishes to replace with a fixed rate. The cost of the existing loan is the risk-free rate + 3%. VW would have to pay a fixed rate of 7% on a fixed rate loan VVVs bank has found a potential counterparty for a swap arrangement.

The counterparty wishes to raise a variable rate loan It would pay the risk-free rate +1 % on a variable rate loan and 8% on a fixed rate.

The bank will require 10% of the savings from the swap and WV and the counterparty will share the remaining saving equally.

Calculate VWs effective rate of interest from this swap arrangement.

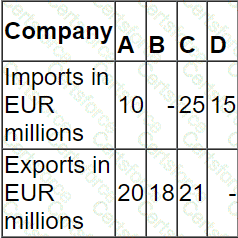

Companies A, B, C and D:

• are based in a country that uses the K$ as its currency.

• have an objective to grow operating profit year on year.

• have the same total levels of revenue and cost.

• trade with companies or individuals in the eurozone. All import and export trade with companies or individuals in the eurozone is priced in EUR.

Typical import/export trade for each company in a year are as follows:

Which company's growth objective is most sensitive to a movement in the EUR/K$ exchange rate?

M is an accountant who wishes to take out a forward rate agreement as a hedging instrument but the company treasurer has advised that a short-term interest rate future would be a better option.

Which of the following is true of a short-term interest rate future?

A company based in Country A with the A$ as its functional currency requires A$500 million 20-year debt finance to finance a long-term investment The company has a high credit rating, but has not previously issued corporate bonds which are listed on the stock exchange Which THREE of the following are advantages of issuing 20 year bonds compared with simply borrowing for a 20 year period?

A private company was formed five years ago and is currently owned and managed by its five founders. The founders, who each own the same number of shares have generally co-operated effectively but there have also been a number of areas where they have disagreed

The company has grown significantly over this period by re-investing its earnings into new investments which have produced excellent returns

The founders are now considering an Initial Public Offering by listing 70% of the shares on the local stock exchange

Which THREE of the following statements about the advantages of a listing are valid?

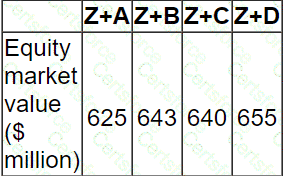

Company Z has identified four potential acquisition targets: companies A, B, C and D.

Company Z has a current equity market value of $580 million.

The price it would have to pay for the equity of each company is as follows:

Only one of the target companies can be acquired and the consideration will be paid in cash.

The following estimations of the new combined value of Company Z have been prepared for each acquisition before deduction of the cash consideration:

Ignoring any premium paid on acquisition, which acquisition should the directors pursue?

Which THREE of the following would be of most interest to lenders deciding whether to provide long-term debt to a company?

An entity prepares financial statements to 31 December each year. The following data applies:

1 December 20X0

• The entity purchased some inventory for $400,000.

• In order to protect the inventory against adverse changes in fair value the entity entered into a futures contract to sell the inventory for a fixed price on 31 January 20X1.

• The entity designated this contract as a fair value hedge of the value of the inventory.

31 December 20X0

• The inventory had a fair value of $480,000 and the futures contract had a fair value of $75,000 (a financial liability).

What will be the impact on the statement of profit or loss and other comprehensive income for the year ended 31 December 20X0 in respect of the change in the value of the inventory and the futures contract?