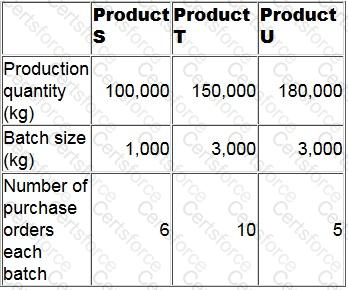

An agricultural company uses activity based costing to charge overheads to its three products. One of the main activities is purchasing, budgeted details of which are as follows:

Additional budgeted data:

What is the budgeted purchasing overhead cost per kg of Product S?

Give your answer to 2 decimal places.

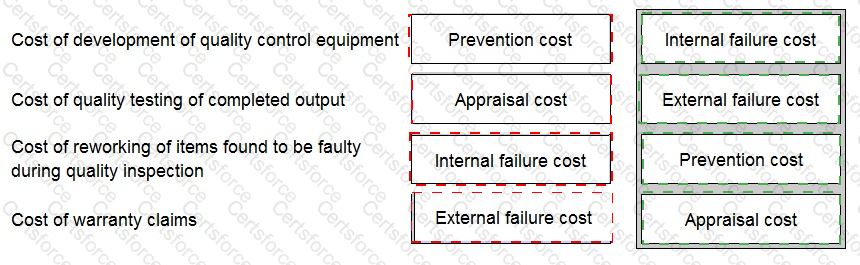

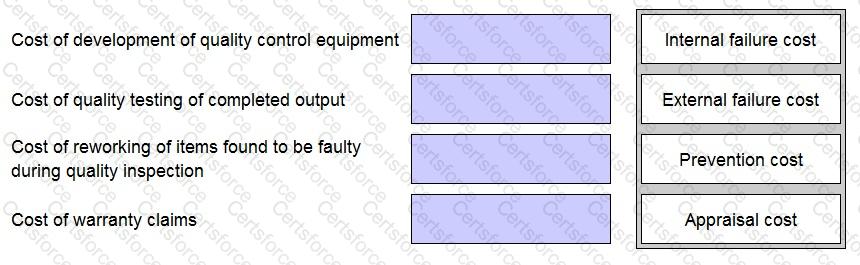

Place the correct label against each item to categorise the cost of the item within the quality cost framework.

Which of the following statements about expected value is NOT correct?

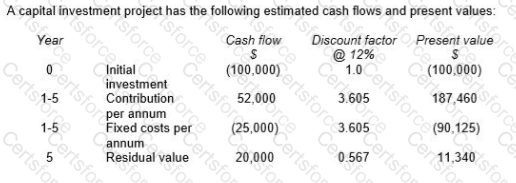

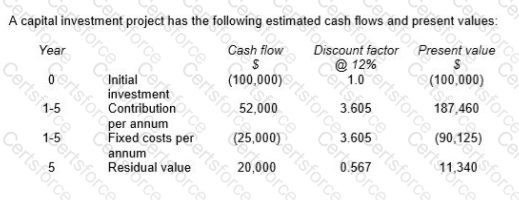

Calculate the sensitivity of the investment decision to a change in the annual fixed costs.

By how much should the present value of the fixed cost increase, before this project is not viable?

A company’s management is considering investing in a project with an expected life of 4 years. It has a positive net present value of $180,000 when cash flows are discounted at 8% per annum. The project’s cash flows include a cash outflow of $100,000 for each of the four years. No tax is payable on projects of this type.

The percentage increase in the annual cash outflow that would cause the company’s management to reject the project from a financial perspective is, to the nearest 0.1%:

Which of the following are examples of feedforward control?

Select ALL that apply.

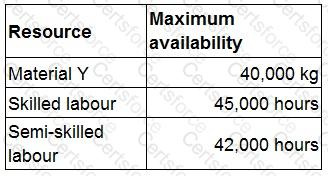

Forecast sales demand of product W next period is 6,800 units. Product W requires 5 kg of material Y, seven hours of skilled labour and six hours of semi-skilled labour.

Availability of resources for next period is forecast as follows:

No inventories are held.

What is the principal budget factor for next period?

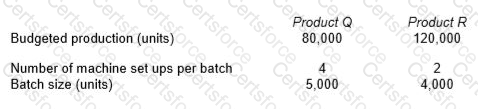

QR uses an activity based budgeting (ABB) system to budget product costs. It manufactures two products, product Q and product R. The budget details for these two products for the forthcoming period are as follows:

The total budgeted cost of setting up the machines is $74,400.

Select TWO potential benefits of using an activity based budgeting system.

Select the benefits to a company of using sensitivity analysis in investment appraisal.

(Select all the true statements.)

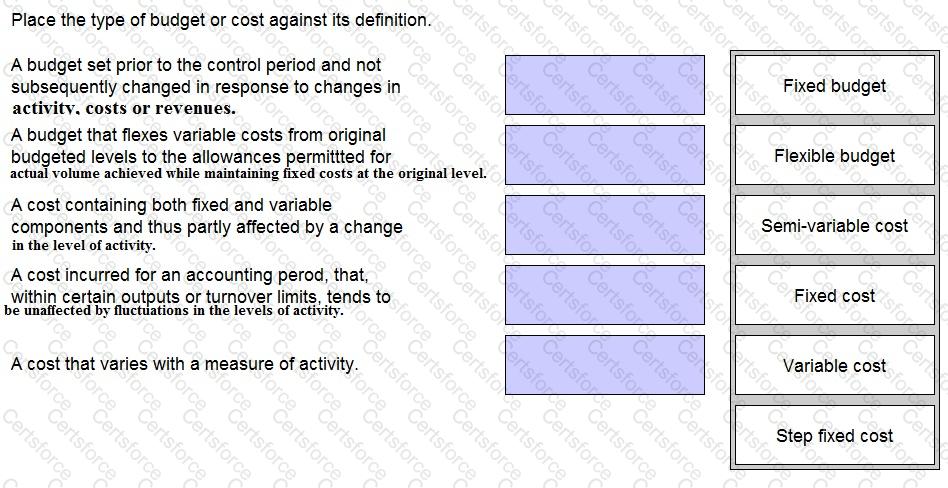

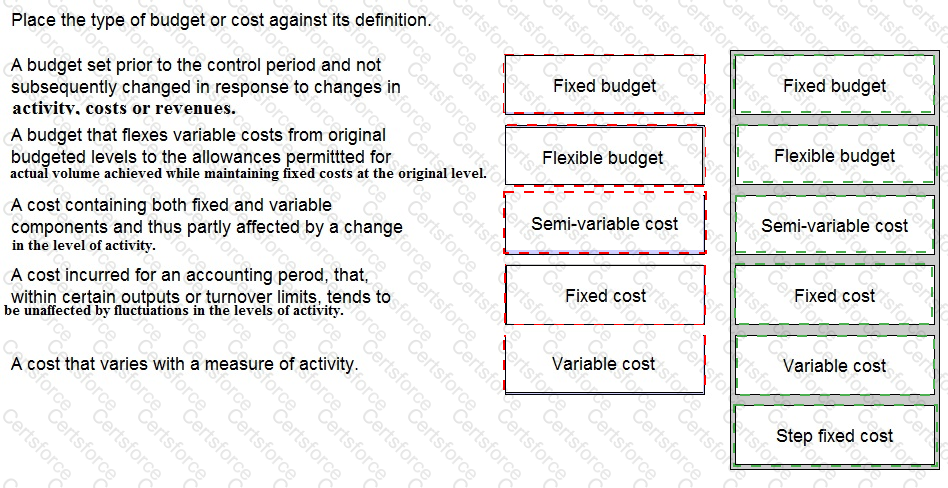

Place the type of budget or cost against its definition.