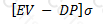

If EV be the expected value of a firm's assets in a year, and DP be the 'default point' per the KMV approach to credit risk, and σ be the standard deviation of future asset returns, then the distance-to-default is given by:

The distance to default is the number of standard deviations that expected asset values are away from the default point. The expression in Choice 'd' represents distance to default. Choice 'd' is the correct answer. The other choices are incorrect.

Contribute your Thoughts:

Chosen Answer:

This is a voting comment (?). You can switch to a simple comment. It is better to Upvote an existing comment if you don't have anything to add.

Submit