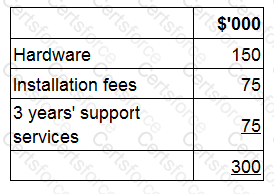

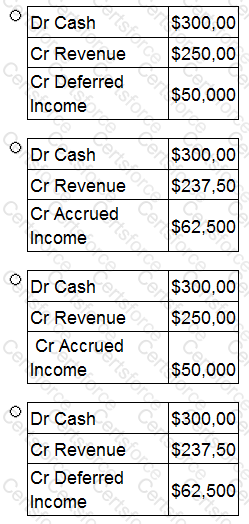

PQ entered into a $300,000 contract on 1 January 20X9 to provide computer hardware to WX with support services for the 3 years from the date of installation.

The contract is made up as follows:

The hardware was delivered to WX on 1 January 20X9 and installed immediately. WX paid the full value of the contract on 30 June 20X9.

What journal entry records PQ's revenue from this contract for the year ended 31 December 20X9?

Which of the following is a related party according to the definition of a related party in IAS24 Related Party Disclosures?

Which of the following should be eliminated when using the equity method to account for associates in a parent's financial statements?

Select ALL that apply.

CD has 200,000 equity shares with a current market value of $2.50 each. The annual dividend of $0.50 a share is about to be paid.

CD also has redeemable debt with a nominal value of $100,000. This is currently trading at $90 for each $100 of nominal value.

The cost of equity is 20% and the post tax cost of debt is 6%.

What is CD's weighted average cost of capital?

Give your answer in % to one decimal place.

? %

Which THREE of the following would typically indicate a finance lease?

ST acquired 80% of the equity shares of AB on 1 January 20X7. AB acquired 60% of the equity shares of UV on 1 January 20X8. Profit for the year ended 31 December 20X9 for AB is $160,000 and for UV is $100,000.

Calculate the non-controlling interest figure to be included within ST's consolidated statement of profit or loss for the year ended 31 December 20X9.

Give your answer to the nearest whole number in $000s.

$ ?

When consolidating for group accounts, a number of calculations and adjustments are required to properly combine the entities into a single group. Which of the following processes are involved in this consolidation

method?

Select ALL that apply:

Which of the following principles are the basic principles followed by the consolidated income statement?

Select ALL that apply.

Which THREE of the following statements are true in relation to financial assets designated as fair value through profit or loss under IAS 39 Financial Instruments: Recognition and Measurement?

AB owned 80% of the equity share capital of FG at 1 January 20X6. AB disposed of 10% of FG's equity share capital on 31 December 20X6 for $400,000. The non controlling interest was measured at $700,000 immediately prior to the disposal.

Which of the following represents the adjustment that AB made to non controlling interest in respect of the disposal when it prepared its consolidated financial statements at 31 December 20X6?