Under the contingent claims approach to credit risk, risk increases when:

I. Volatility of the firm's assets increases

II. Risk free rate increases

III. Maturity of the debt increases

Which of the following are a CRO's responsibilities:

I. Statutory financial reporting

II. Reporting to the audit committee

III. Compliance with risk regulatory standards

IV. Operational risk

An assumption regarding the absence of ratings momentum is referred to as:

What would be the consequences of a model of economic risk capital calculation that weighs all loans equallyregardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capitalrequirements

The frequency distribution for operational risk loss events can be modeled by which of the following distributions:

I. The binomial distribution

II. The Poisson distribution

III. The negative binomial distribution

IV. The omega distribution

A risk management function is best organized as:

When compared to a medium severity medium frequency risk, the operational risk capital requirement for a high severity very low frequency risk is likely to be:

When combining separate bottom up estimates of market, credit and operational risk measures, a most conservative economic capital estimate results from which of the following assumptions:

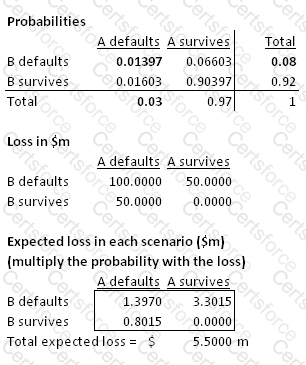

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the default correlation is 25%, what is the one year expected loss on this portfolio?

Loss from a lawsuit from an employee due to physical harm caused while at work is categorized per Basel II as: