There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that none of the three bonds will default.

Which of the following risks and reasons justify the use of scenario analysis in operational riskmodeling:

I. Risks for which no internal loss data is available

II. Risks that are foreseeable but have no precedent, internally or externally

III. Risks for which objective assessments can be made by experts

IV. Risks that are known to exist, but for which no reliable external or internal losses can be analyzed

V. Reducing the complexity of having to fit statistical models to internal and external loss data

VI. Managing the capital estimation process as to produce estimates in line with management's desired capital buffers.

For a loan portfolio, expected losses are charged against:

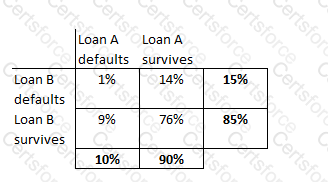

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. Theprobability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

What would be the correct order of steps to addressing data quality problems in an organization?

According to the Basel framework, shareholders' equity and reserves are considered a part of:

Which of the following are considered properties of a 'coherent' risk measure:

I. Monotonicity

II. Homogeneity

III. Translation Invariance

IV. Sub-additivity

Which of the following belong to the family of generalized extreme value distributions:

I. Frechet

II. Gumbel

III. Weibull

IV. Exponential

For a group of assets known to be positively correlated, what is the impact on economic capital calculations if we assume the assets to be independent (or uncorrelated)?

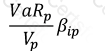

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above