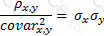

A portfolio manager desires a position of $10m in physical gold, but chooses to get the exposure using gold futures to conserve cash. The volatility of gold is 6% a month, while that of gold futures is 7% a month. The covariance of gold and gold futures is 0.00378 a month. How many gold contracts should he hold if each contract is worth $100k in gold?

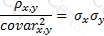

The relationship between covariance and correlation for two assets x and y is expressed by which of the following equations (where covarx,y is the covariance between x and y, σx and σy are the respective standard deviations and ρx,y is the correlation between x and y):

A)

B)

C)

D)

None of the above

What is the running yield on a 6% coupon bond selling at a clean price of $96?

Which of the following cause convexity to increase:

I. Increase in yields

II. Increase in maturity

III. Increase in coupon rate

IV. Increase in duration

Continuously compounded returns for an asset that increases in price from S1 to S2 over time period t (assuming no dividends or other distributions) are given by:

Credit risk in the case of a CDO (Collateralized Debt Obligation) is borne by:

A currency with a lower interest rate will trade:

The dates on which the interest rate applicable to the floating rate leg of an interest rate swap is determined are called

For an investor short a bond, which of the following is true:

I. Higher convexity is preferable to lower convexity

II. An increase in yields is preferable to a decrease in yield

III. Negative convexity is preferable to positive convexity

Arrange the following rates in descending order, assuming an upward sloping yield curve:

1. The 10 year zero rate

2. The forward rate from year 9 to 10

3. The yield-to-maturity on a 10 year coupon bearing bond

103.11.e1 is the standard deviation of the asset to be hedged, and

103.11.e1 is the standard deviation of the asset to be hedged, and  103.11.e2 is the standard deviation the asset being used to hedge against price movements in x, then the minimum variance hedge ratio is given by the expression

103.11.e2 is the standard deviation the asset being used to hedge against price movements in x, then the minimum variance hedge ratio is given by the expression  103.11.e3. In this question, correlation = 0.00378/(6%*7%) = 0.9. The minimum variance hedge ratio is given by (6%/7%)*0.9 = 0.77

103.11.e3. In this question, correlation = 0.00378/(6%*7%) = 0.9. The minimum variance hedge ratio is given by (6%/7%)*0.9 = 0.77 103.11.a3

103.11.a3