BCD's finance cost for the year ended 30 June 20X6 in its statement of profit or loss is $198,000. BCD's statement of financial position is as follows:

How much will be included in BCD's statement of cash flows for interest paid in the year ended 31 December 20X6?

Give your answer to The nearest $.

XYZ operates in Country P where the tax rules state entertaining costs and accounting depreciation are disallowable for tax purposes.

In year ending 31 March 20X4, XYZ made an accounting profit of $240,000.

Profit included $14,500 of entertaining costs and $5,000 of income exempt from taxation.

XYZ has plant and machinery with accounting depreciation amounting to $26,300 and tax depreciation amounting to $35,200.

Calculate the taxable profit for the year ended 31 March 20X4.

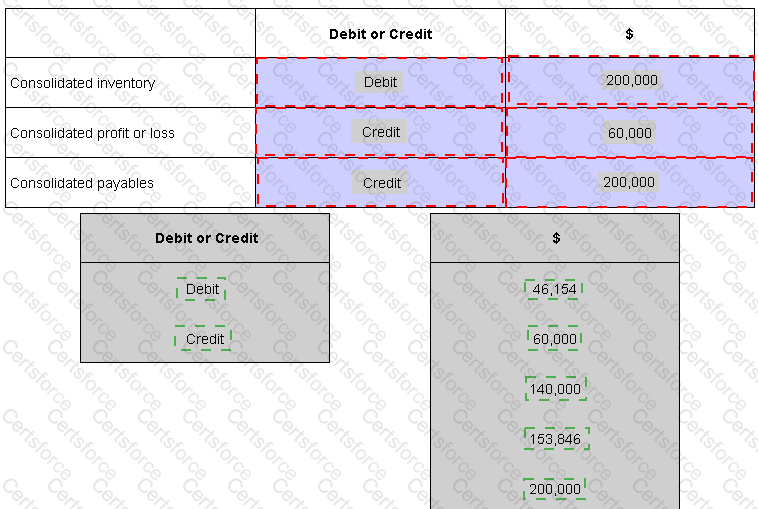

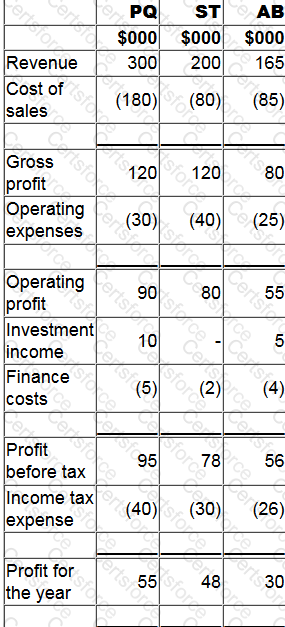

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September 20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

Calculate the amount that will be shown as the share of profit of associate in PQ's consolidated statement of profit or loss for the year ended 31 December 20X0.

WX is considering an investment in ST.

At 31 December 20X2 ST had the following balances in its statement of financial position:

Which of the following would cause ST to become an associate investment of WX?

UV's financial statements for the year ended 31 March 20X8 were approved for publication on 30 June 20X8.

In accordance with IAS 10 Events After the Reporting Period, which of the following material events would have been classified as a non-adjusting event in these financial statements?

Which of the following would NOT be considered an element of a regulatory framework for financial reporting?

Which of the following is NOT a responsibility of the International Accounting Standards Board?

AB has prepared its financial statements for the year ended 31 July 20X5. On 15 September 20X5 a major fraud was uncovered by the external auditors which had taken place during the year to 31 July 20X5 The financial statements have not yet been authorised

In accordance with IAS 10 Events After the Reporting Period, AB should treat the fraud as:

The International Accounting Standards Board's "The Conceptual Framework for Financial Reporting" identifies fundamental and enhancing qualitative characteristics of financial statements.

Which of the following is included within the fundamental characteristics?