In accordance with IAS 1 Presentation of Financial Statements, which of the following will be shown in the statement of changes in equity?

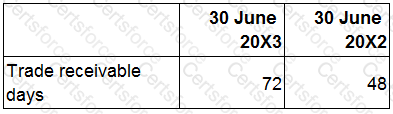

The following information relates to ABC.

Which of the following would be a reason for the movement in the trade receivable days?

Which THREE of the following statements about government grants are INCORRECT?

Country J is a newly formed independent country and it's accounting professionals are considering adopting international financial reporting standards (IFRS).

Which of the following is a disadvantage to Country J of adopting IFRS as their local generally accepted accounting practice (GAAP)?

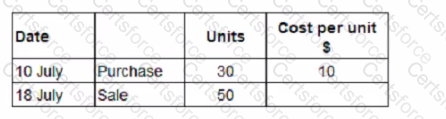

On 1 July 20X8 JKL has 100 units of inventory, which cost $8 each. The following transactions arose during the month of July:

JKL values inventory using the first in. first out method.

What is the value of JKL's inventory at 31 July 20X8?

Give your answer to the nearest $.

In accordance with IAS 16 Property, Plant and Equipment, in which of the following situations would subsequent expenditure on a non-current asset be capitalised?

In an entity's statement of profit or loss and other comprehensive income, which of the following would be presented as other comprehensive income?

XYZ operates in Country A where tax rules state that entertaining costs and donations to political parties are disallowable for tax purposes.

XYZ calculated both its accounting and taxable profits for the year ended 31 December 20X2 after deducting $10,000 of entertaining costs.

It is considering what impact the ruling that "entertaining costs are disallowable for tax purposes" will have on its two profit figures.

Which of the following correctly states the impact of the ruling on the profits already calculated?

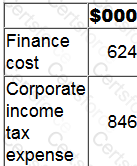

The following information is extracted from QQ's statement of financial position at 31 March:

Included in other payables is interest payable of $80,000 at 31 March 20X2 and $73,000 at 31 March 20X1.

The following information if included within QQ's statement of profit or loss for the year ended 31 March 20X2.

Included within finance cost is $124,000 which relates to interest paid on a finance lease. QQ includes finance lease interest within financing activities on its statement of cash flows.

QQ is preparing its statement of cash flows for the year ended 31 March 20X2.

What cash outflow figure should be included for corporate income tax paid within the cash flow from operating activities section of the statement?

Give your answer to the nearest $000.

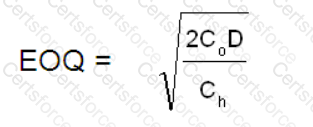

Refer to the exhibit.

An entity sells 2,000 bags of product X each year. It has been estimated that the cost of holding one bag of product X is £4.

The cost of placing an order is £250.

where:

Co = cost of placing an order

Ch = cost of holding one unit in inventory for one year

D = annual demand

Calculate the Economic Order Quantity (EOQ) for bags of product X.

Give your answer to the nearest whole number of bags.